The State of the Ecommerce Fashion Industry: Statistics, Trends & Strategies to Use in 2022

by

The fashion industry is no stranger to innovation. 2PM reports that 13 of the top 20 DTC brands are in the fashion and apparel industry. Brands like Skims, Allbirds, and Gymshark make the shortlist, proving the crushing power fashion brands hold in the ecommerce space.

Digital innovation, rising globalization, and changes in consumer spending habits have catapulted the fashion industry into the midst of seismic shifts. But, no thanks to the accelerated retail apocalypse caused by the coronavirus, the fashion sector is more unpredictable than ever.

This guide shares the statistics, trends, and strategies shaping the ecommerce fashion market in 2022 and beyond, giving you an updated look on where we are and where we’re heading.

Ecommerce fashion industry: statistics

1. Industry-wide data

According to Statista, the ecommerce fashion industry’s compound annual growth rate (CAGR) is tipped to reach 14.2% between 2017 and 2025, with the industry hitting a $672.71 billion valuation by 2023.

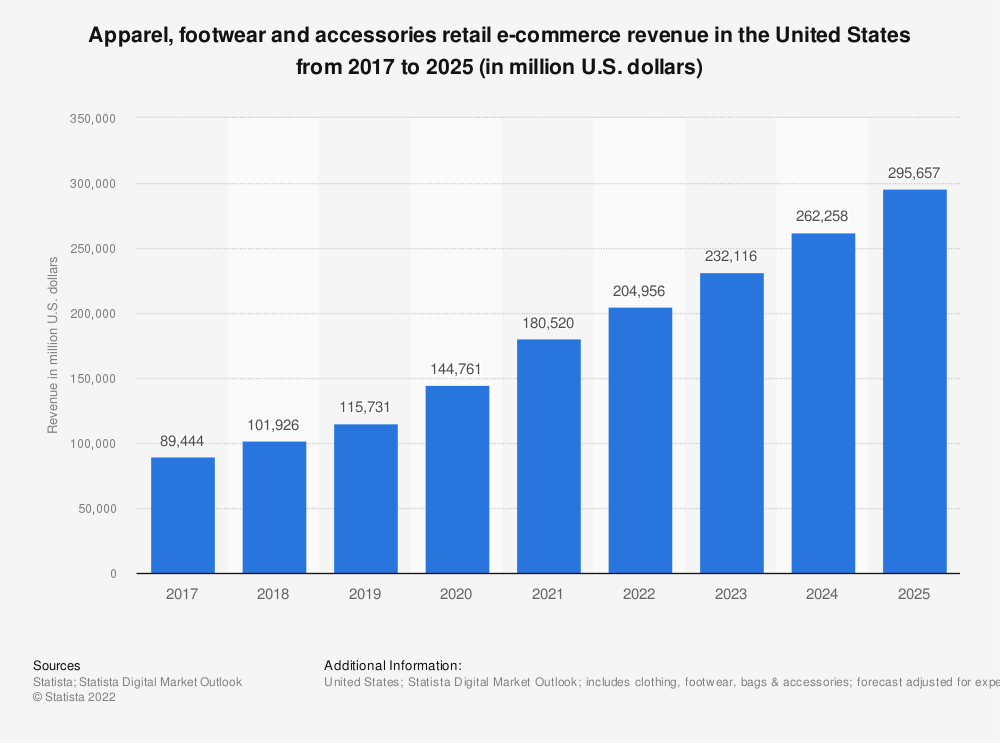

Sales of apparel, footwear, and accessories catapulted in 2021, hitting $180.5 billion in the US alone. That’s tipped to grow by 13% this year, with consumers set to spend $204.9 billion on fashion items online.

Driving this growth are five notable opportunities:

- Expanding global markets outside the West

- Increasing online access and smartphone penetration

- Emerging worldwide middle classes with disposable income

- Harnessing the power of celebrity and influencer culture

The biggest threats to established brands include:

- The death of brand loyalty due to market saturation

- Pressure from consumers to use ethically sourced and green manufacturing materials

- Technological advancements with virtual worlds, such as NFTs and the metaverse

We’ll get into strategies to combat these issues later. For now, let’s examine how these big numbers play out in industry sub-verticals.

2. The COVID impact

The coronavirus pandemic wreaked havoc on the last few years’ fashion ecommerce predictions. When lockdowns were enforced globally in March 2020, 27% of US consumers said they planned to spend “somewhat” or “a lot” less on luxury and fashion items than they had budgeted prior.

Despite this, McKinsey named it the “perfect storm for fashion marketplaces.” Brands like Zalando reported a 32% to 34% growth in gross merchandise value (GMV) during the second quarter of 2020. Fast-fashion brand Shein saw its valuation double to $30 billion, making it the world’s largest online-only fashion retailer.

One branch of fashion retail that has taken off is athleisure. Athleisure’s market size was valued at $155.2 billion in 2018—a figure that’s set only to rise.

Casualwear remains dominant on Amazon, with athleisure predicted to have a CAGR of 6.7% from 2019 to 2026 and reach $257.1 billion. The loungewear and sleepwear market shows similar signs of growth, poised to increase by $19.5 billion between 2020 to 2024.

The result? Fashion brands with an ecommerce store maintain a stronghold in athleisure, like Nike and Lululemon, have reported incredible growth over the course of the pandemic.

3. Clothing and apparel

Lower digital barriers to entry for all clothing merchants offer the opportunity to market, sell, and fulfill orders globally and automatically. As a result, worldwide revenue and revenue per user (ARPU) are both projected to grow.

In the US alone, the apparel and accessory industries accounted for 29.5% of all ecommerce sales in 2021. In Europe, it’s expected that by 2025, each consumer will spend $999 on fashion-related items over the course of a year.

4. Shoes segment

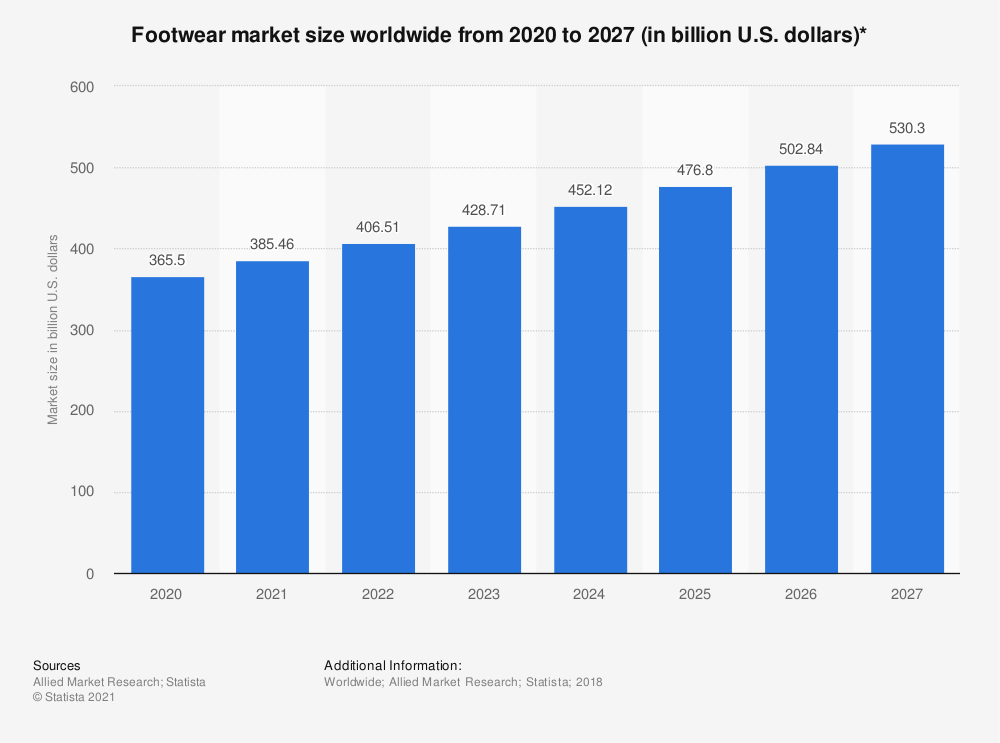

As a segment of ecommerce fashion, the shoe industry saw similar peaks in market value. In global market size, the footwear segment will increase from $365.5 billion in 2022 to $530.3 billion in 2027.

Asia is dominating this segment, holding 54% of the global footwear market (compared to just 14.8% for Europe and North America, respectively).

Athletic footwear is also a growing segment, tipped to generate $63.5 billion in 2023—a 23% increase from the $51.4 billion valuation in 2020.

5. Accessories and bags

Not surprising, the bags and accessories segment—although still growing at a stronger rate—will likewise see double-digit growth. The fashion accessory segment will have a CAGR of 12.3% between 2016 and 2026, with Asia-Pacific being the fastest growing market.

Those projections actually make bags and accessories one of the healthiest segments of ecommerce fashion, despite its absolute numbers being the smallest.

6. Jewelry and luxury

In 2020, the global jewelry market was valued at a total of $228 billion. It’s forecasted to reach $307 billion by 2025, with ecommerce sites expected to facilitate 20.8% of sales in the luxury goods category this year. Luxury watches are set to take a huge slice of that revenue—customers will spend $9.3 billion on them in 2025.

The growth (despite coronavirus-related recessions) mirrors other financial crises. McKinsey predicted that consumers will “return more quickly to paying full price for quality, timeless goods, as was the case after the 2008–2009 financial crisis.”

Increasing affluence in Asia-Pacific and in the Middle East drove up the average revenue per luxury good consumer to $313. Despite luxury goods sales seeing sluggish growth, at 3.4% annually, McKinsey forecasts indicate that ecommerce could triple in sales over the next decade—reaching €70 billion ($79.5 billion) by 2025.

The biggest threat is the affordable luxury market: Should the industry offer luxury goods at multiple price points to grow the market overall? Or will affordable luxury dilute or erode the high-end luxury market—dampening consumer confidence that what they are buying is “true luxury”?

Ecommerce fashion industry: trends and strategies for 2022

The above data points offer a wealth of growth opportunities for fashion and apparel retailers—despite the huge shifts in consumer behavior, global trade, and “normal” day-to-day lives for millions around the world.

Below are some of the latest ecommerce trends that you can work into your long-term fashion sales strategy.

- Personalization is a balancing act

- Into the metaverse

- Brand-building over paid ads

- Sustainability at the forefront

- Social commerce

- The transition back to brick-and-mortar

Personalization is a balancing act

Personalization has long been hailed as the secret of modern ecommerce. By showing items a shopper was previously interested in, or retargeting them based on the activity they’ve had with your ecommerce website, you’re providing a tailored online shopping experience—one that convinces them to buy.

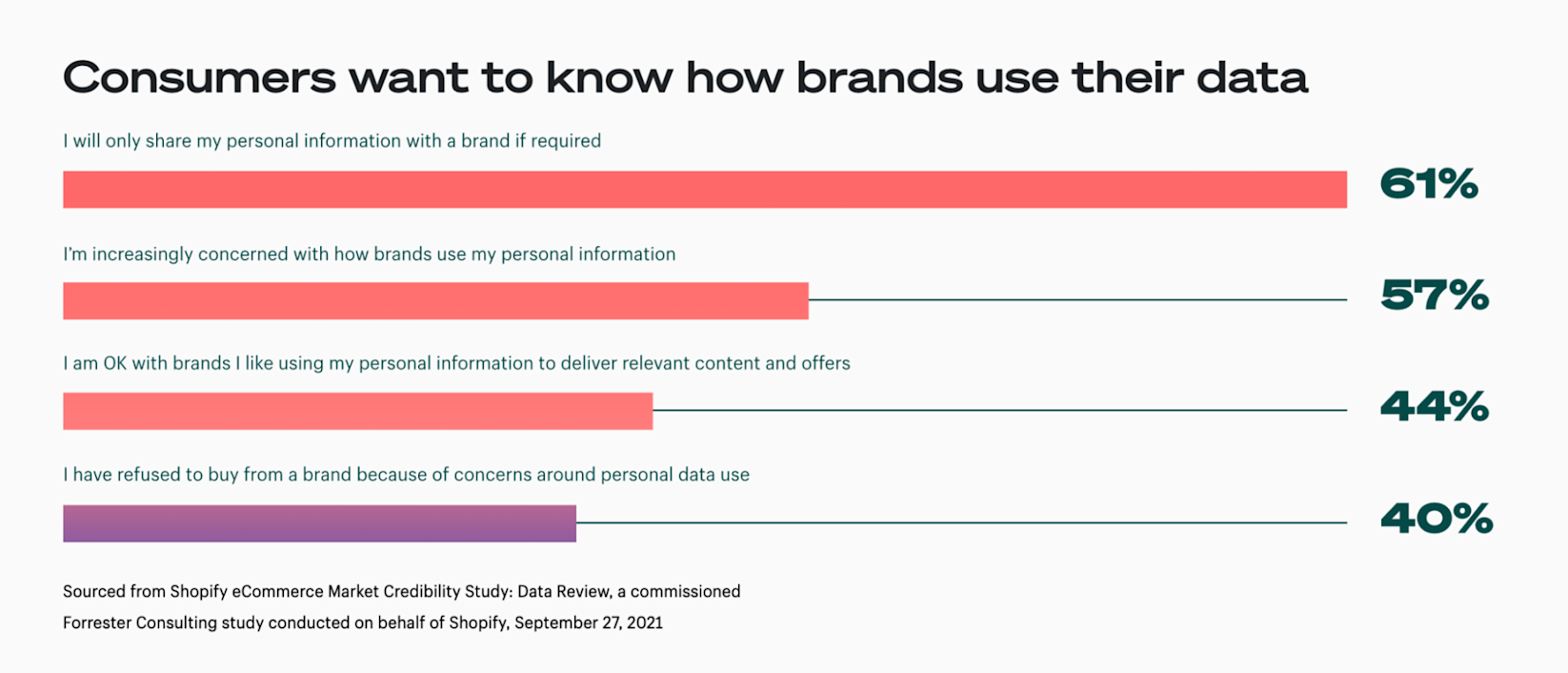

Our research shows that 44% of customers are OK with brands using their personal information to personalize messaging and improve the customer experiences, such as product recommendations. But there’s a fine line.

Online shoppers are increasingly concerned about their privacy. Too much personalization can be creepy, hence why brands that over-personalize are three times more likely to be abandoned by shoppers.

Culture Kings is the perfect example of how fashion ecommerce brands can balance under- and over-personalization. Instead of customizing the experience down to “first name” tags on the website, it built four global storefronts to sell in different currencies. The result? More than half of the fashion brand’s revenue now comes from its ecommerce business.

"I believe we'll see more local brands branching out and offering customized shopping experiences for international customers to remain competitive. This will include things like geo-targeted domains, pricing in local currency and local product shipping, with the help of third-party distribution or company owned warehouses.”

—Leanne Lee, Marketer at Blue Bungalow

Into the metaverse

The definition of “metaverse” is open to interpretation. The not-quite-defined promise of virtual societies is still in development, though the idea is that people can conduct daily activities—like connecting with friends, playing a game, and purchasing products—through an online, virtual world.

One type of item that functions both in and out of the metaverse are non-fungible tokens (NFTs)—unique digital tokens that can only be owned by one person, usually paid for in virtual currency like crypto. Data shows $87.03 million was spent on NFTs on January 1, 2022, alone.

Celebrities like Reese Witherspoon were mocked for predicting, “In the (near) future, every person will have a parallel digital identity. Avatars, crypto wallets, [and] digital goods will be the norm.”

In everything we do, we’re helping the customer imagine. We want them to imagine being the man in every picture. To imagine us being their stylist. To imagine, ‘That could be me wearing those clothes.’ We’re not so much curating content as curating imagination.”

—Kevin Dao, Co-founder and CEO/CCO at ORO LA

In reality, fitness apparel brands like Under Armour are experimenting with NFTs in the retail space. Its Steph Curry collaboration reproduced shoes the basketball star wore when he broke the NBA record as all-time top three-point shooter.

Digital NFTs were released alongside the physical product launch. Owners of the NTFs could virtually wear the shoes in three metaverses: Decentraland, The Sandbox, and Gala Games.

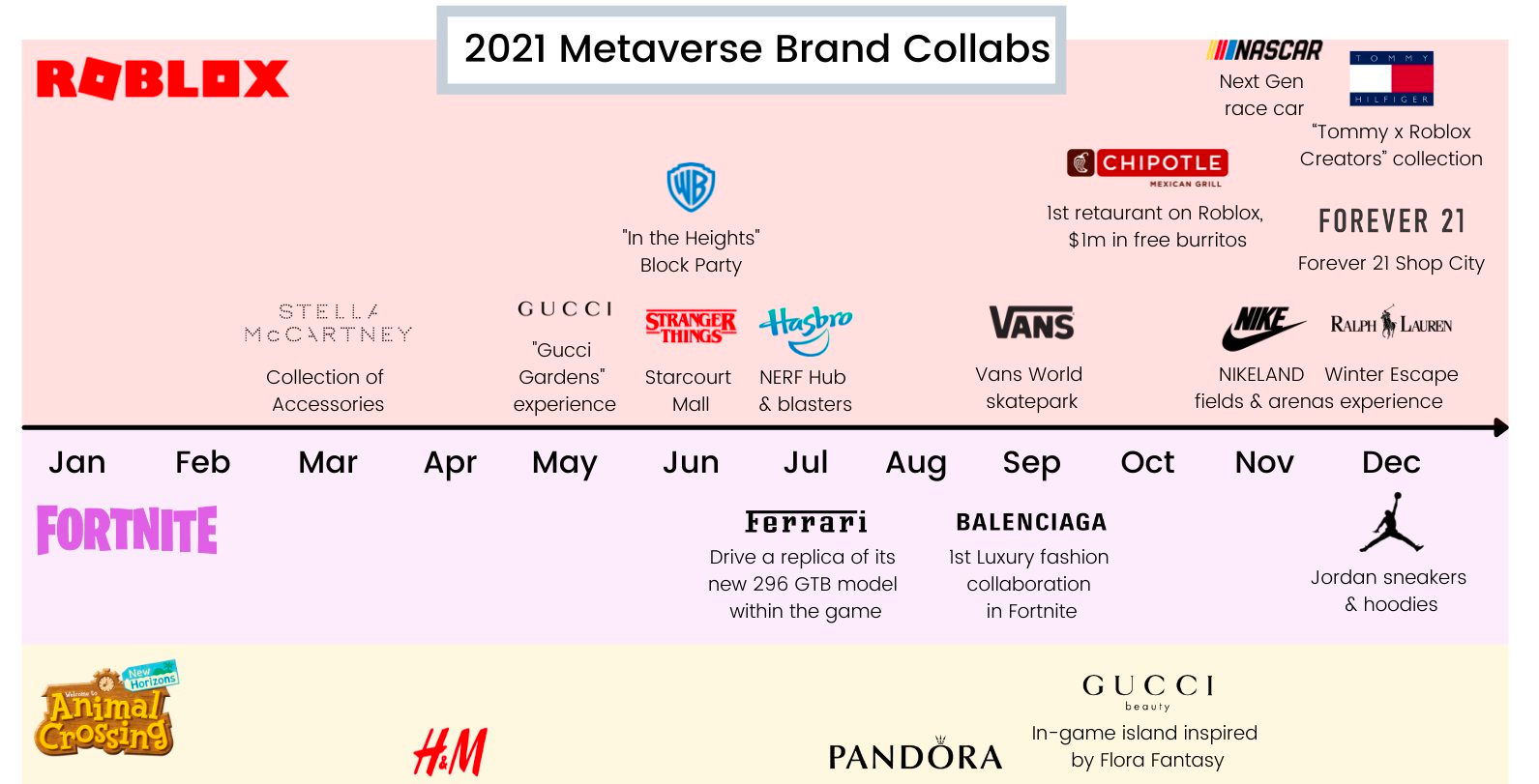

Retailer Forever 21 partnered with Roblox to create virtual stores in its metaverse, appropriately named the Forever 21 Shop City. Players run the virtual store as if it was their own, and purchase merchandise for their avatar through the game.

With Forever 21 Shop City, our goal is to expand how we engage with customers, extending our presence and product in new ways.”

—Katrina Glusac, chief merchandising officer at Forever 21

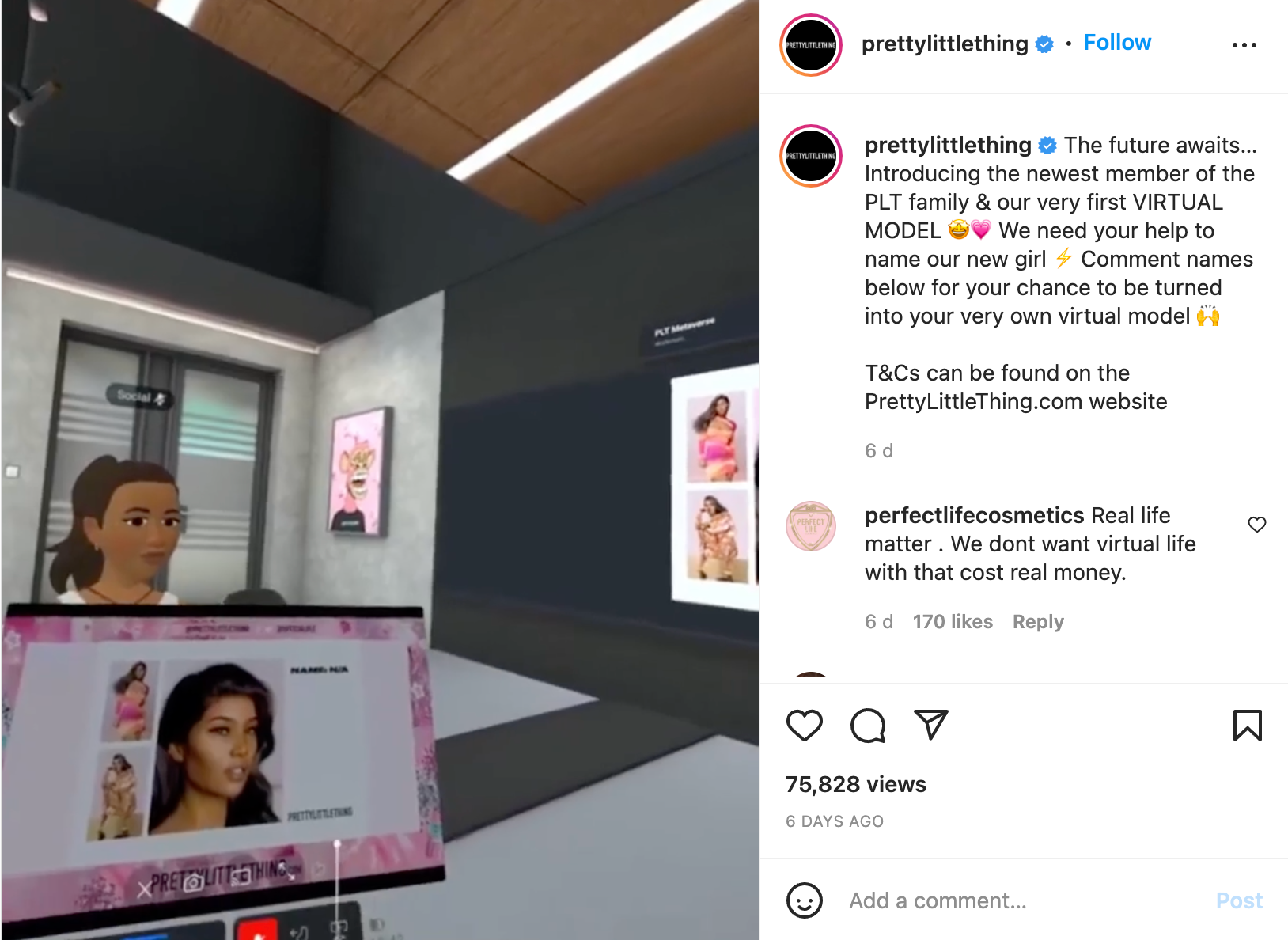

Fast-fashion retailer PrettyLittleThing also recently began showcasing products on virtual models. The brand posted the news to its Instagram page, turning its new “avatar in the metaverse” concept into a competition to spark conversation.

Just like Fortnite community inspired Balenciaga’s designs, fashion companies can move towards becoming creative collectives. Each collection can have its own identity within the brand universe, reputation, and community. Collectives can focus on the actual product designs and/or on content creation, with associated royalties based on item/content performance, delivering returns to creators in perpetuity and ensuring that a brand attracts the very top talent.”

—Ana Andjelic, Founder of The Sociology of Business

Brand-building over paid ads

To say fashion ecommerce is saturated would be an understatement. Consumers have more choice than ever before—making it difficult to drive loyal customers back to one particular online store.

Unfortunately, that means brands are competing against thousands of competitors when advertising their products to their target market. Some 41% of brands plan to increase their investment in paid search. This rush of budget meant that between the second and third quarters of 2021, the cost per click (CPC) of paid search ads increased by 15%.

It’s an increasingly bleak picture when combined with the “death of the cookie.” Technology giants like Google plan to restrict brands from collecting cookies in its browser by 2023. Some 28% of technology decision makers expect this change in regulation to hinder their 2022 growth goals.

One alternative to expensive advertising and limited customer data? Brand building. Studies show companies that invest in branding see more organic acquisition and customer retention rates. They also find it easier to increase profits since customers of strong brands are more receptive to price hikes.

One apparel brand leaning into this strategy is Noémie. Yuvi Alpert, its founder, Creative Director, and CEO, says the brand balances both performance marketing and brand building: “We wanted to move away from typical short form advertising that did not draw an emotional connection to our products, which is why we diversified our promotions and the channels we utilized to feature narrative ads.

“Narrative or storytelling promotions had share rates of up to 20%, and in recognizing this fact, we decided to research the best ways to implement that strategy.

“By creating storylines about our customers, and then placing those in content rich formats such as blogs, newsletters, and emails, we found dramatic increases in engagement rates over the typical banner ads or short videos on social media.

“In addition, they were far more cost effective and could easily be repurposed. By moving to a storytelling technique, we increased engagement rates while bringing down our CPA.”

Sustainability at the forefront

The fashion industry is no stranger to criticism. Fast-fashion brands especially are (sometimes rightly) chastised for the methods they use to manufacture and produce inventory.

In light of these criticisms making mainstream news, plus consumers’ increasing commitment to eradicate climate change, some 52% of shoppers say they’re more likely to purchase from a company with shared values.

An important value for modern fashion consumers? Sustainability. Statista’s research shows 42% of global customers purchase eco-friendly and sustainable products. Certain countries are leading the trend—online shoppers in Vietnam, India, and the Philippines purchase sustainable products more often.

With people spending more time online, it is going to facilitate faster exchange of that information [about suppliers]. We’ve become more aware of how things that happen in far flung places affect us and the planet. That’s been a real key change we’ve seen.”

—Grace Beverly, Founder of TALA

Purchasing habits are also shifting off the back of the pandemic. Some 65% of customers plan to purchase more durable fashion items, with 71% planning to keep the items they already have for longer. The fashion resale market is booming for this reason—growing 11 times faster than traditional retail and tipped to reach a $77 billion valuation in the next five years.

Patagonia is one apparel brand with sustainability rooted in its brand values. The retailer actively campaigns for environmental causes, and demonstrates its commitment to sustainability with its Worn Wear program. Shoppers are encouraged to buy and sell used items instead of buying new.

We’re proud to offer our customers a conscious shopping choice with sustainable, affordable pieces that are all handpicked and on trend, but we believe every brand needs to take responsibility, and push themselves to become more circular.”

—Kate Peters, Managing Director of Beyond Retro

Social commerce

Social media plays an integral role in the ecommerce marketing strategy of many online fashion brands. That’s hardly surprising—our smartphone addiction is out of control. The typical social media user now spends about 15% of their waking life glued to an online networking app.

But the truth is: social media is no longer a place for shoppers to consume new fashion trends. Many social media platforms are evolving their business models to facilitate in-app shopping, helping online retailers reach customers actively in the purchasing frame of mind.

Social commerce sales are expected to nearly triple by 2025, with more than one-third of Facebook users planning to make a purchase directly through the platform in 2022.

Unfortunately, most brands are plagued by a single sin. Andy Crestodina, co-founder of Orbit Media, describes the situation perfectly: “Most branded content is advertising under a thin layer of information or entertainment. Scratch the paint, find an ad. It’s the brand putting itself first.”

Thankfully, fashion and social media are a match made in ecommerce heaven. Even when it comes to explicitly “branded” content, and especially on Instagram.

Social media engagement rates for global fashion brands are abysmal:

- Instagram: 0.68%

- Facebook: 0.03%

- Twitter: 0.03%

So, what types of content is working for fashion brands? Some 46% of consumers want to watch product videos before they buy. Platforms like TikTok and Instagram are praised for driving sales for large fashion brands since shoppers can visualize the product on a real person. Bonus points if it’s a social media influencer they already trust.

Long gone are the days of celebrities being only someone you’d see on TV. Today, anyone with a passion can become a celebrity in the social media niche—partly due to the rise of entertainment platforms like Instagram, LinkedIn, and Twitch.

Beyond influencer marketing on social media, multi-channel ecommerce integrates native selling off site to build direct buying paths in the places your audience spends their time. Social media platforms are creating their own commerce features—like Shopping on Instagram, Facebook Shops, buyable pins on Pinterest, and more.

Livestream shopping is also in its heyday. Nordstrom launched its own livestream shopping channel last year. It’s in good company: 81% of companies plan to increase or maintain their investment in livestream selling to drive sales over the coming year.

Why? Because online brands are seeing conversion rates of up to 30% through Facebook and Instagram livestreams, along with lower product return rates.

My prediction is that in a couple years, the hottest role for a brand to hire is going to be a head of live shopping.”

—Kevin Gould, Co-founder of Glamnetic

The transition back to brick-and-mortar

The shopping experience is more complex than ever—especially in the fashion space. Some 22% of online returns happen because the product ordered online looks differently in the flesh. It’s this never-ending challenge that’s driving many fashion brands back into traditional retail.

The future is neither ecommerce or retail. It’s just commerce. So the question becomes, ‘How do you symbiotically integrate both channels?’”

—Hemant Chavan, founder of Brik + Clik

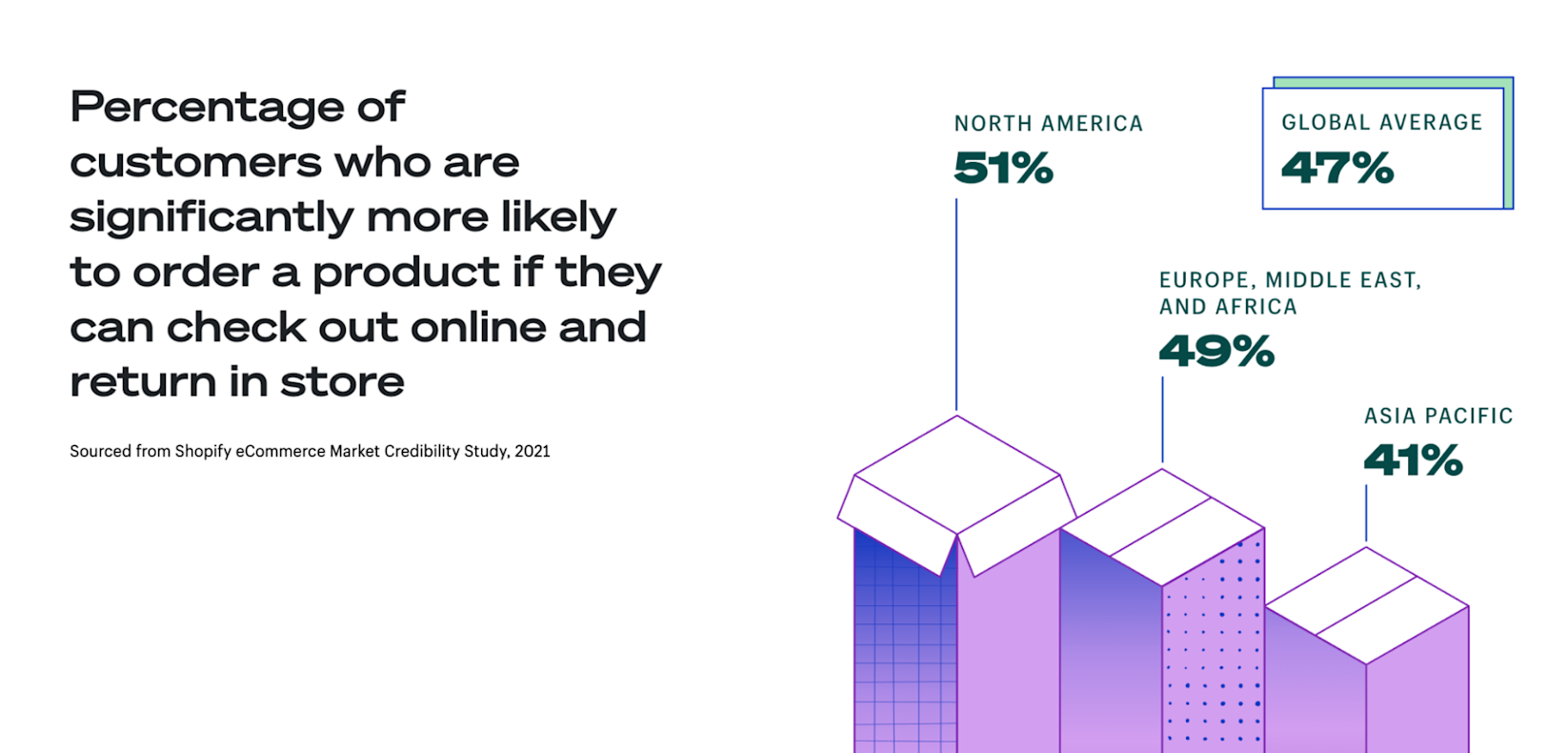

Data compiled in the Future of Commerce report proves omnichannel commerce isn’t disappearing anytime soon. Modern consumers want both online and offline sales channels—and synergy between the two:

- 54% of consumers are likely to look at a product online and buy it in a physical store.

- 53% vision themselves doing the opposite: viewing products in-store and buying it online.

- 55% of consumers want to browse products online and check what’s available in local stores.

- Over 50% of adult shoppers use BOPIS, with 67% adding extra items to their carts when they can pick them up immediately.

Brands investing in brick-and-mortar retail include Canadian fashion brand SMYTHE, which opened its store in Toronto. After years of experimenting with pop-up shops, Gymshark also opened its first permanent flagship store in central London.

“A children’s wear retailer I spoke to pivoted from in-store events to virtual shopping events via Zoom during COVID,” says Kyle Monk, Director of Insight, British Retail Consortium.

“Suddenly, they were having one member of staff walking around the store selling products to two to 300 people per call every week, instead of just a few in person. Retailers who thought innovatively and pivoted thrived over the last period.”

It’s no wonder 53% of brands are investing in tools that allow them to sell anywhere.

Want more about the state of ecommerce fashion?

The state of ecommerce fashion is developing more quickly than ever. What worked two years ago is outdated now—largely due to consumer preferences changing, values becoming integral to the purchase decision, and footfall returning to brick-and-mortar stores.